As the remote and hybrid work models remain highly popular among employers and employees alike, the coworking industry continues to grow and evolve across the nation. With this in mind, we leveraged proprietary data from the fourth quarter of 2023 to break down the coworking landscape in the 25 largest U.S. markets and get a better understanding of the coworking sector’s current state and historic evolution.

Then, we compared the most recent data with the state of the industry in Q3 of 2023, also looking at national-level prices, the total coworking inventory, the square footage covered by it and the leading operators currently on the market.

National Coworking Supply Continues Upward Trajectory, New Jersey Registers Highest Q-o-Q Growth

The national coworking inventory reached a total of 6,251 flex workspaces at the end of 2023. With the total supply at 6,172 spaces in Q3, this represented a slight increase of 1.28% in the span of three months. Although the quarter-over-quarter (Q-o-Q) increase is not major, it does signal a stabilization of the coworking market. However, what’s more significant is that the vast majority of the top 25 markets saw increases in their total coworking inventories during Q4 of 2023. The most prominent was registered in New Jersey, where 13 more coworking spaces were opened in one quarter for an increase of 9% since the end of Q3.

Notably, during the last three months of 2023, just one-fifth of the top 25 markets registered slight losses in their coworking inventories, and even the most significant of these dropped only 2% in Washington, D.C., Seattle and Minneapolis-St. Paul. As such, the markets now stand at 247, 123 and 85 coworking spaces, respectively. At the same time, Manhattan lost three coworking spaces in Q4 (from the previous 270) for a 1% decrease in coworking supply, while Chicago saw a very slight drop of 0.4% after just one coworking space closed in the span of three months (now logging 229).

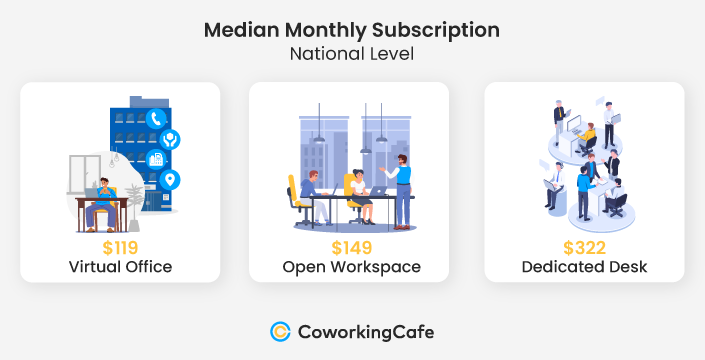

Rates for Open Workspaces Remain Stable, Virtual Offices & Dedicated Desks More Affordable in Q4

In terms of pricing, the national median rate for virtual offices in Q4 was $119, which was slightly lower than it was at the end of Q3, when it stood at $125. Once again, Washington, D.C. still registered the lowest median among all of the 25 top markets — only $80, which was exactly the same as it was in Q2 and Q3 of 2023. Similarly, four other markets also stood below the $100 mark in the virtual office category — Denver, Miami, Orange County, CA, and Brooklyn.

At the other end of the spectrum, Chicago and New Jersey came in significantly above the national median rate for virtual offices at $205.

Meanwhile, the national median rate for open workspaces remained the same in Q4 as it was in Q3 at precisely $149 per month. However, this type of coworking subscription also varied significantly with Manhattan reaching $225 and other popular markets — like Washington, D.C. and San Francisco — charging $200 for the same type of membership.

That said, Phoenix and Orange County, CA, were at the opposite end, coming in below the national median rate for open workspaces at a more affordable $119 — exactly the same as in the previous quarter.

Interestingly, dedicated desks went down in price from a national median of $329 in Q3 to $322 at the end of Q4. Even so, in Chicago and Salt Lake City, dedicated desks were at the $269 mark — below the national median. The second-most affordable rate in this category was in the Dallas-Fort Worth market, at $271.

As expected, Manhattan was still significantly above the national rate at $520. Nearby in Brooklyn, dedicated desks were also on the more expensive end with a median of $455, whereas the same type of coworking membership cost $442 in San Francisco.

Leading Markets by Number of Coworking Spaces

Los Angeles Takes Lead with Highest Number of Spaces, Surpassing Manhattan

While Los Angeles stood behind Manhattan at a difference of three coworking spaces in Q3, LA has now surpassed the Big Apple for the first time in months — albeit by exactly one space: in Los Angeles, the coworking inventory gained one more coworking space in Q4 (now standing at a total of 268 spaces), while Manhattan registered a slight 1% decrease, going from 270 flex workspaces to 267.

Otherwise, New Jersey, Brooklyn and Austin logged surges of 9%, 7% and 6%, respectively, in their total numbers of coworking spaces — the highest increases among the top 25 markets. In New Jersey, the inventory went up from 137 spaces in Q3 to 150 at the end Q4 to place the market in the 10th spot nationally.

Next, after previously securing the third spot in terms of coworking supply, Washington, D.C. was surpassed by Dallas-Fort Worth in Q4, which grew its inventory by 3%, while that attributed to the nation’s capital decreased by 2%. Accordingly, DFW now stands at precisely 249 coworking spaces, while D.C. claims 247.

Likewise, a slight 2% decrease in inventory was also registered during Q4 in Seattle and Minneapolis-St. Paul, and a minor drop of just one coworking space (the equivalent of -0.4%) was seen in Chicago. Despite this, 20 of the top 25 U.S. markets saw increases in their numbers of coworking spaces, which shows healthy growth in the sector across the nation.

Leading Markets by Square Footage

Philadelphia & New Jersey Gain Most Coworking Ground in Q4, with 11% Increases in Total Square Footage

Despite registering a slight decrease in the total square footage on a national level in Q3, the coworking sector appears to have stabilized in the last three months of 2023. Specifically, the national square footage allocated to flex workspaces increased by 3% in Q4, rising from 117.7 million square feet to 120.8 million.

Although almost all of the top markets increased their coworking footprints in Q4, Philadelphia and New Jersey experienced the most significant growth in square footage. In both of these markets, we registered 11% increases in the total surface covered by coworking spaces, which put Philadelphia at 2.5 million square feet and New Jersey at 2.4 million. Not to be outdone, Fort Lauderdale also logged a significant increase of 7% in square footage during Q4, which placed it back in the top 25 markets after being previously overturned by Indianapolis. As a result, the Fort Lauderdale market held up the end of the rankings, but with a solid 1.3 million square feet of coworking space.

In the same way, Brooklyn also increased its square footage by 7% to surpass the 2.3-million mark. Other markets that logged notable growth in coworking surfaces were Miami (6% Q-o-Q) and Nashville (5%).

It’s worth noting here that only two of the top 25 markets logged decreases in the total square footage covered by coworking spaces in Q4 — and even those were minor: the Raleigh-Durham market lost 2% of its total coworking surface to finish at 1.8 million square feet, and Manhattan lost 1% of its total coworking square footage. Even so, Manhattan still leads in this category with almost double the surface covered by runner-up Los Angeles (12.6 million square footage in Manhattan, as opposed to 6.6 million in LA).

Most Markets Increase Average Square Footage, but Austin’s Drops by 5%, Showing Focus on Smaller Coworking Spaces

Despite the fact that only two markets lost total coworking square footage, seven of the top 25 saw decreases in their average square footage. This goes to show that, in many cases, smaller coworking spaces are gaining popularity. Granted, most of these markets registered very minor changes, such as -0.1% in Houston; -0.3% in Manhattan, San Francisco and Salt Lake City; and -2% in San Diego. Raleigh-Durham also lost 3% of its average square footage in Q4. Yet, with the exception of San Diego, all of these markets still stood above the national average of 19,331 average square feet.

Plus, Manhattan still led in terms of coworking space surface with a whopping 47,000 average square footage (more than double the national average). It was followed at a distance by Brooklyn and San Francisco.

However, Austin, Texas, saw a 5% decrease in Q4 of 2023, dropping from an average of 23,000 square feet to slightly below 22,000 — despite seeing very minor changes in the total square footage attributed to its coworking inventory. Moreover, with four new spaces added in the last three months of the year, coworking in Austin is clearly gravitating toward smaller spaces. Thus, in this category, the market lost two positions in the ranking, going from 9th place to 11th, right behind Seattle and the Bay Area.

Distribution of Top Coworking Operators

HQ Joins Leading Operators, After Doubling Its Inventory in Only 3 Months

In Q4, industry giants Regus, WeWork, Industrious and Spaces held onto their leading positions by checking the highest number of coworking spaces — both on a national level and among the top 25 markets. However, this quarter, Premier Workspaces — which, in Q1, Q2 and Q3 of 2023 was the fifth-most popular operator in the country — was surpassed by HQ.

In the span of just three months, HQ saw impressive growth in its portfolio after doubling its national coworking supply and growing by more than 200% among the top 25 markets. Consequently, the operator now owns 167 spaces across the U.S., 78 of which are located in leading markets.

Finally, Regus managed to register 2% growth nationally and 1% growth among the leading markets to hold onto its #1 position. Additionally, Industrious and Spaces maintained the same inventory among the 25 markets, but Industrious grew by 1% nationwide, while Spaces decreased by 1%. Unfortunately, WeWork continued its downward trajectory, losing 3% of its coworking spaces located in the top markets. Moreover, the operator decreased by 4% Q-o-Q on a national level, falling from 195 spaces in Q3 to only 188 at the end of Q4.

Methodology

- To compile this report, we used proprietary data from CoworkingCafe to determine the number of coworking spaces per market, as well as the total square footage and the leading operators.

- The study relied solely on the listing data available on CoworkingCafe as of January 2024.

- The top 25 markets analyzed were established per our sister company, Yardi Matrix and ranked based on allocated square footage.

- In terms of pricing, we looked at the national median starting prices per person per month for virtual office, open workspace and dedicated desk coworking subscriptions.

Fair Use & Redistribution

We encourage and freely grant you permission to reuse, host or repost the images in this article. When doing so, we only ask that you kindly attribute the authors by linking to CoworkingCafe.com or this page so that your readers can learn more about this project, the research behind it and its methodology.