Key Takeaways:

- The podium remained unchanged since 2023 with New York City in the lead despite a 10% reduction in the number of coworking spaces across Midtown Manhattan and the Financial District.

- Washington, D.C. closed in on Chicago from a difference of 17 central business district (CBD) coworking spaces to just one space shy of the silver medal.

- Philadelphia climbed to fourth place by number of CBD coworking spaces in 2024 to overtake Los Angeles.

- The coworking scene exhibited overall stability with growth focused outside of the central business districts.

- Half of all U.S. downtown coworking spaces were concentrated in just eight major CBDs.

With work culture prioritizing flexibility and a sense of community now more than ever, the coworking model represents the best fit for the needs of many modern-day office workers. But, even with suburban flex workspaces continuing to crop up as a professional alternative to the home office, coworking spaces did not entirely break free from the “location, location, location” mantra. Rather, business districts remain a sought-after market for operators, especially in the major commercial and economic hubs where prohibitive office prices fuel demand for membership-based solutions among startups, SMBs and even enterprise clients that have adopted a flexible workstyle.

With this in mind, we ranked the U.S. cities with the highest numbers of flexible office spaces within their business districts. In addition, we also looked at the one-year evolution of the distribution of coworking hubs within these economic powerhouses.

8 Business Districts Cluster Half of All CBD Flex Spaces With Coastal Hubs in the Lead

Although most top CBDs saw a contraction in their coworking offer in the last year, the podium remained unchanged and fluctuations were more moderate further down the list. Accordingly, the top-heavy distribution carried over to 2024 with a slight correction: While half of all U.S. CBD flexible workspaces were concentrated in the top five business districts in 2023, this year that halving point slid further back. Specifically, in 2024, more than 370 of the roughly 720 centrally located flex spaces were spread across eight CBDs. Notably, part of the reason for the attrition is that early adopters are typically also the ones that see the first and most significant drops as markets mature and consolidate.

In terms of geographical distribution, the East Coast — particularly the Northeastern region — maintained its lead and further strengthened its dominance with Pittsburgh entering the top 10. At the same time, the large economic powerhouses of California and Texas remained in a deadlock with the Lone Star State gaining a slight advantage as Houston closed in on Los Angeles. Meanwhile, Chicago held out as the sole representative of the Midwest among the top CBDs for coworking.

Downtown Focus Wanes as Coworking Market Expands Outside Business Districts

As we’ll see in some of the most prominent examples below, business districts have lost some traction in the last year, but the overall coworking scene nevertheless exhibited stability with urban and suburban dynamics taking the lion’s share in shaping the growth of the sector. However, although WeWork started shedding weight years before its bankruptcy announcement last November, the industry-wide influence of such a significant event cannot be ignored, especially in strategic locations like the central business districts. Still, the rate at which the competition has been scooping up WeWork’s vacated spaces suggests that the drop might prove to be temporary in many key markets.

Same CBDs Remain on Podium, But Fluctuations Set Stage for Close Race

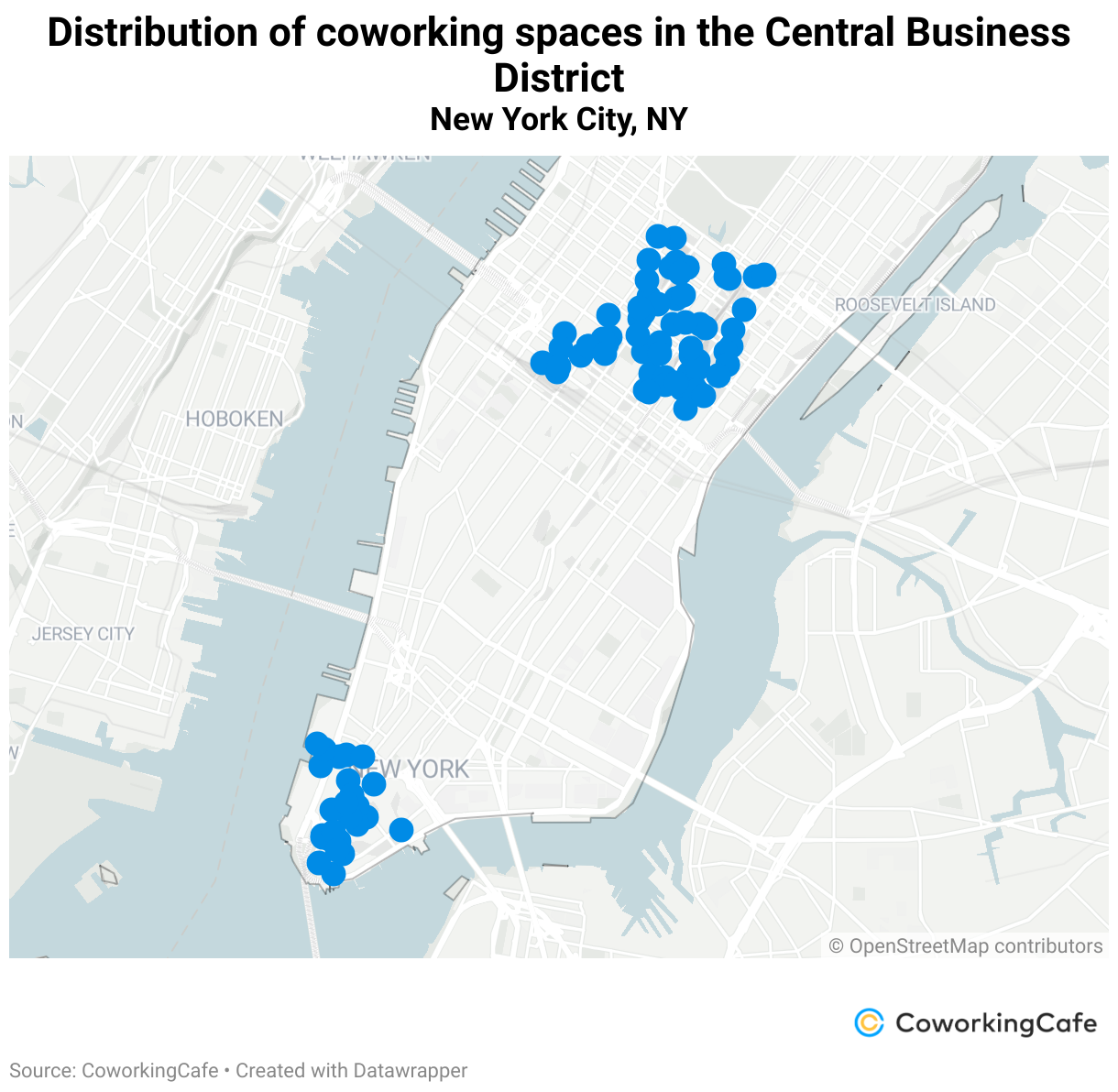

New York City, NY remains the ultimate coworkers’ playground with more than 160 flex workspaces in Midtown Manhattan and the Financial District alone, as well as almost 360 in all five boroughs — 20 more than last year. However, even as it maintained its pole position and substantial head start over any other U.S. market, The Big Apple also saw the largest drop in the number of coworking spaces in its business districts: NYC totaled 17 less than it did in 2023 to mark a roughly 10% contraction of its CBD inventory. Even so, the city’s #1 spot in this ranking should remain safe for the foreseeable future.

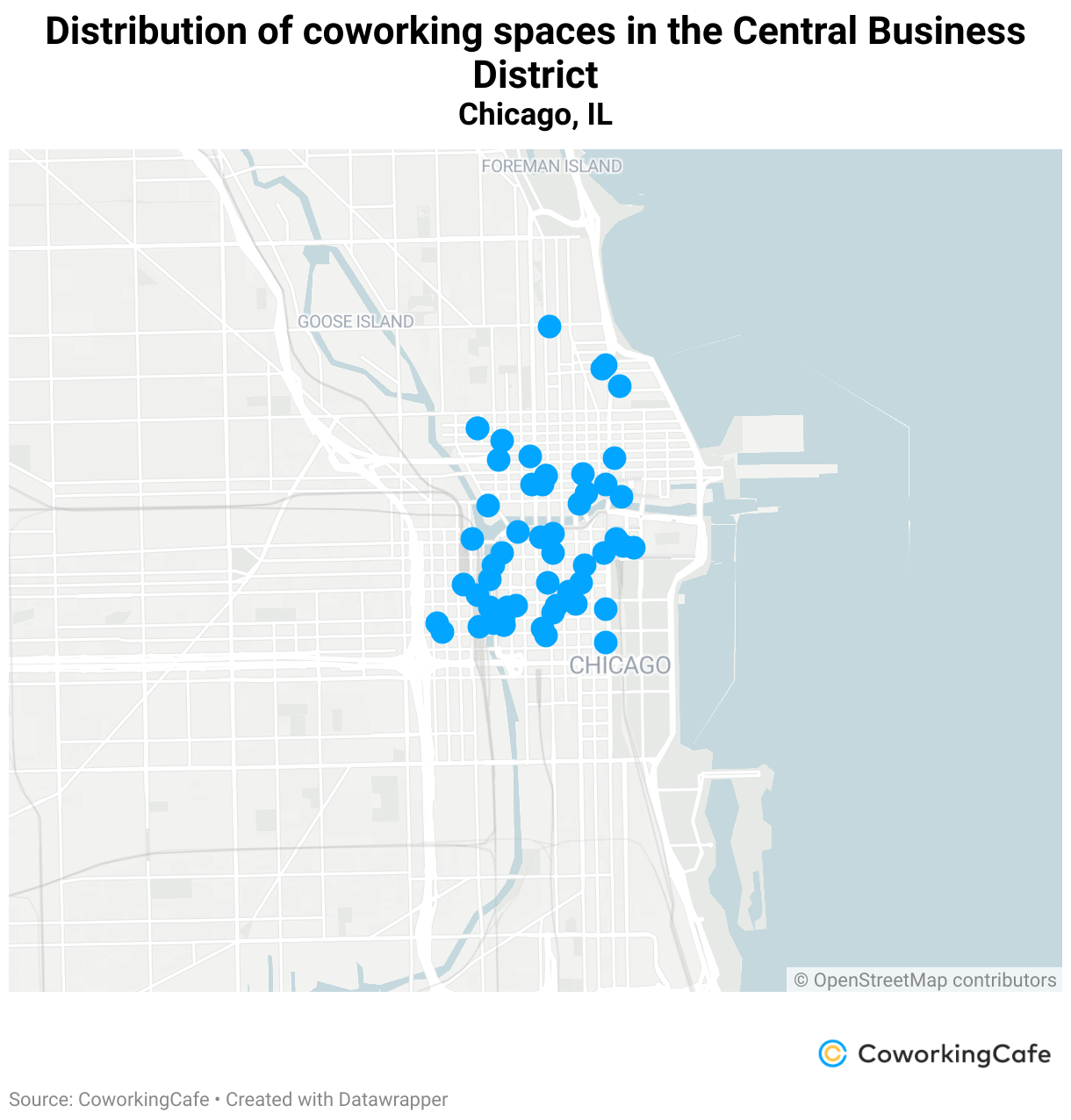

In the middle of the country, Chicago, IL counts 55 coworking spaces in and around the Loop that represent more than half of the city’s total inventory. However, this means 16 fewer spaces than last year, which is an even more significant difference than New York’s 17 considering the proportions. Plus, while there was moderate growth in other parts of the city, it wasn’t enough to offset the sudden nosedive in the downtown area, which now counts 98 flexible workspaces throughout the city — down from 107 in 2023.

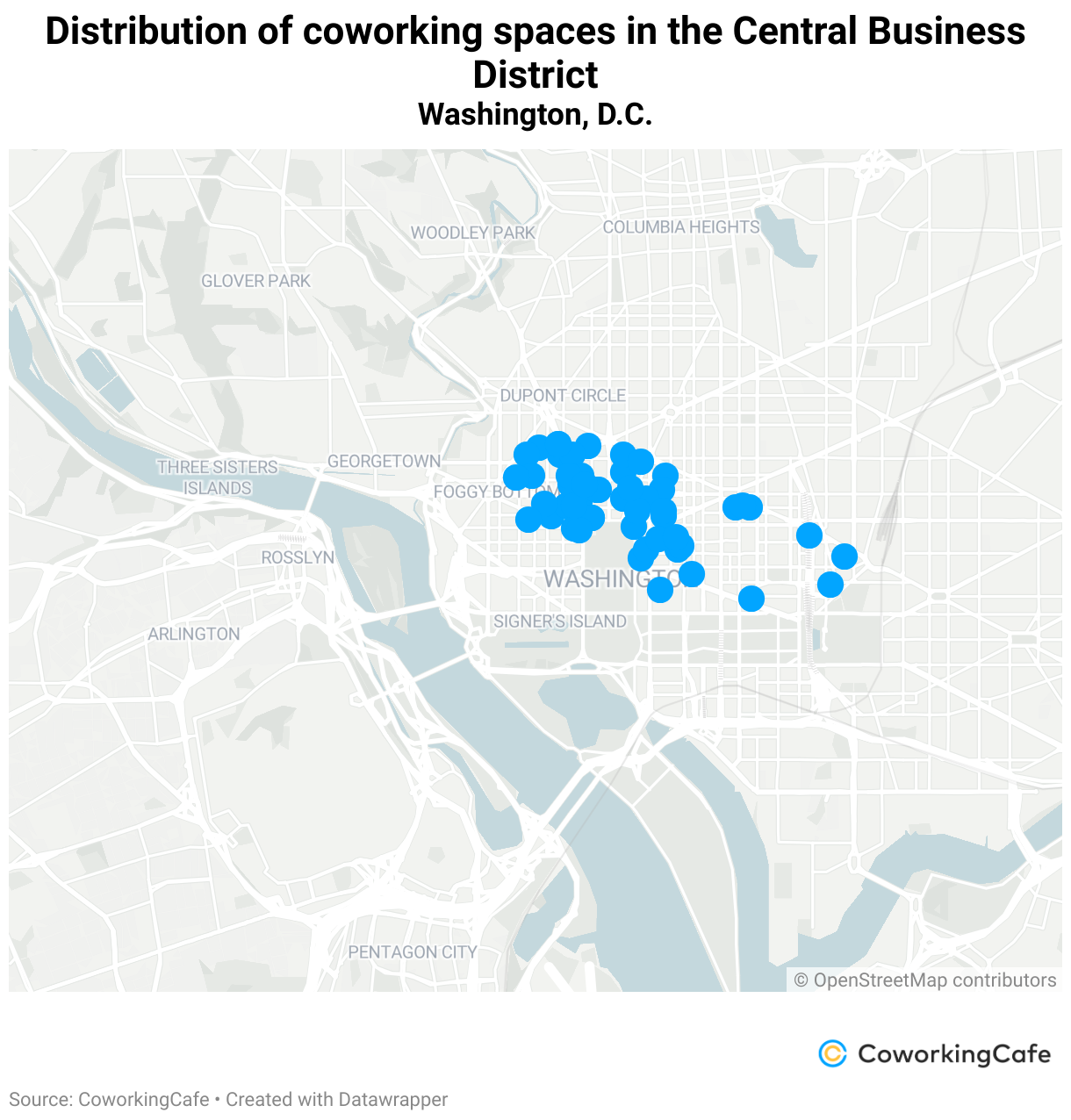

Next — and in the context of the retreat seen throughout the last year as the coworking segment continued to consolidate in the largest local economies — the fact that Washington, D.C. held on to all 54 of its CBD flex spaces is no small feat. Instead, this stability is indicative of a mature market, and the high concentration within the business district (69%) further highlights the continued appeal of flexible work solutions for government agencies, NGOs and advocacy groups. It’s also worth noting that all of these factors — coupled with the significant shift in Chicago — put D.C. within a hair’s breadth of second place, so it should be interesting to follow the future development of the city’s downtown coworking scene.

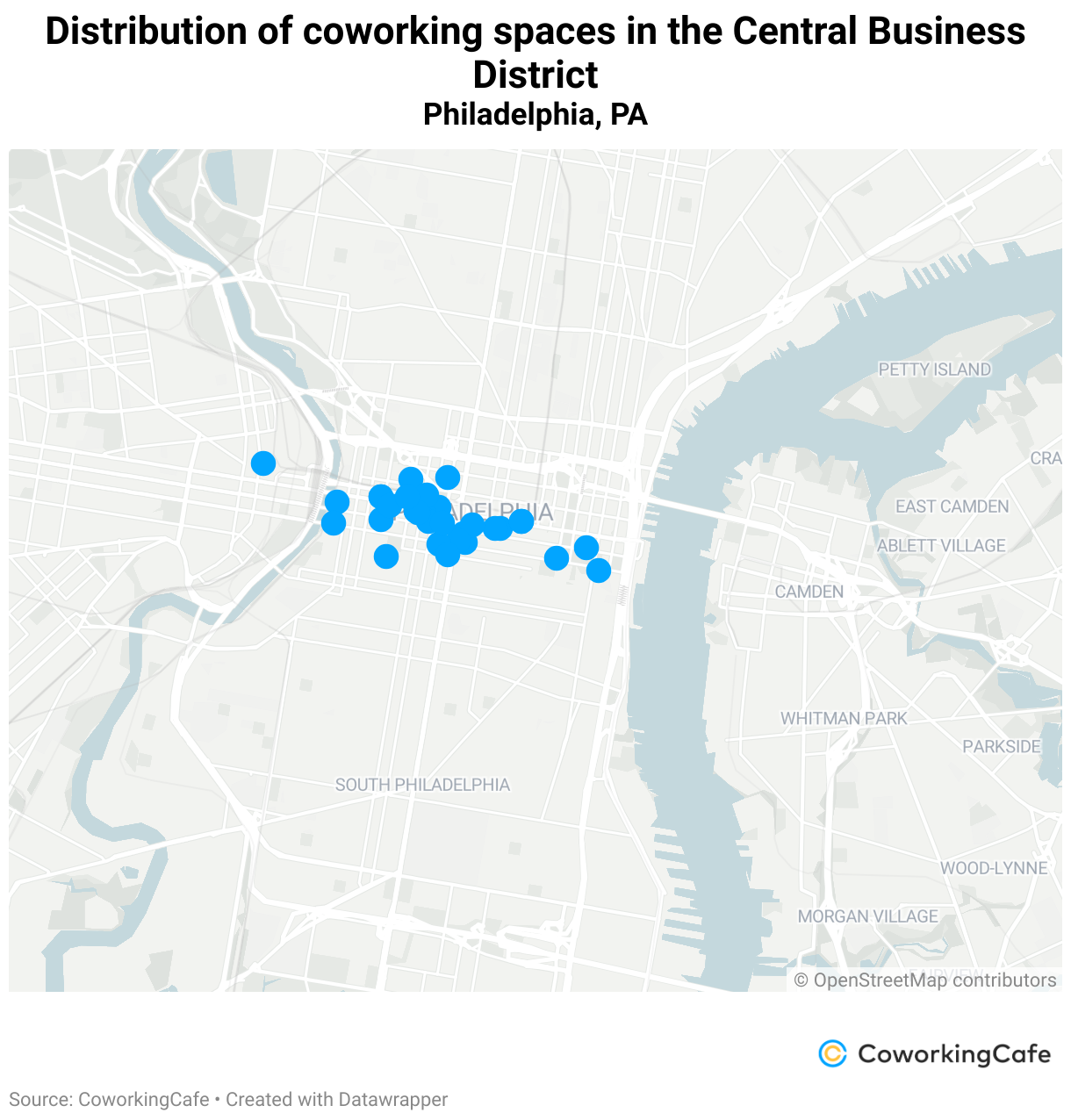

Notably, Philadelphia, PA climbed one spot to fourth place thanks to five new flexible workspaces opening in the CBD and another five in other parts of the city. Here, Philly has 32 of its 51 flex spaces located in the Center City area — a 63% share that also places the city among the most downtown-focused coworking markets.

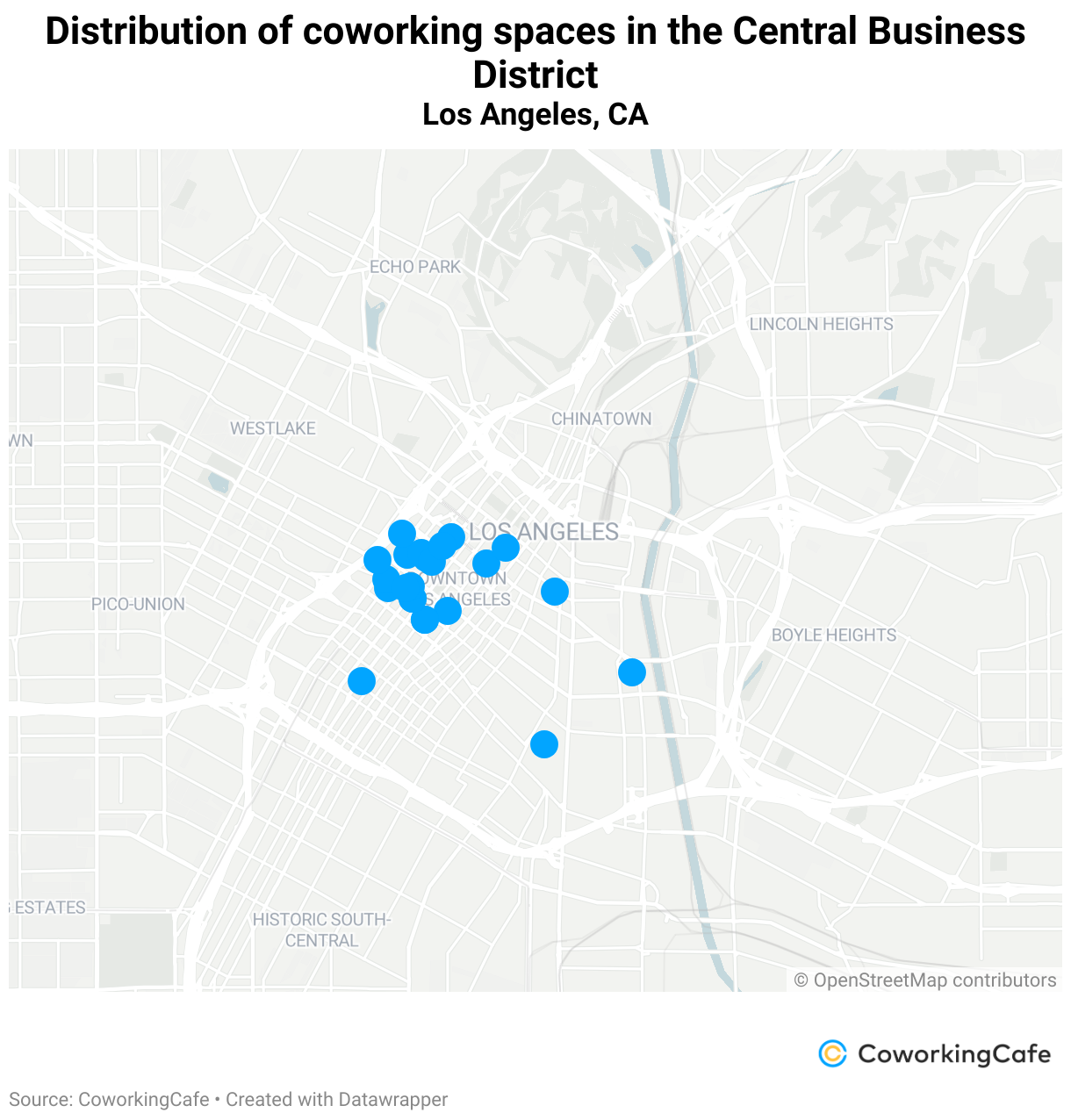

On the opposite coast — and boasting a total of 75 coworking offices in 2024, almost one-third of which (23) are located in the CBD — Los Angeles, CA came in fifth in the ranking, sliding back one place since last year. Because LA’s inventory dropped both in the CBD and other parts of the city, the reduction was relatively uniform with 31% of its coworking inventory remaining in the CBD. In this case, six of the 19 flex workspaces removed were in downtown.

East Coast Stays Prominent in Lower Half of Top 10; Texas & California in Close Competition

The number of CBD coworking spaces in Houston increased by four since last year to bring the total to 19. Downtown Houston, TX seems to be a rising star with the past year’s progressions suggesting that it might even challenge LA for the coworking crown in the Sun Belt, and already has more flex workspaces than San Francisco’s CBD. Additionally, Houston is one of the few cities on the list that registered a slight inward migration with the number throughout the entire city flat year-over-year, pushing the share of downtown coworking spaces to 13%.

To the east and now home to 14 coworking spaces, downtown Orlando, FL added just one more coworking space to its inventory. Still, this moderate progress, coupled with the decreases seen in other cities, meant that Orlando climbed two places on the leaderboard to #7. At the same time, the total number of flex spaces dropped by 14 spaces, representing the second-largest overall reduction after Los Angeles. This also means the coworking market has become more downtown-focused, with 45% of the inventory now concentrated in the CBD — up from 29% last year.

Back on the West Coast, San Francisco, CA posted significant overall growth with 17 new spaces throughout the city for a total of 64. However, there are now only 13 flex workspaces in the CBD — three less than last year. This places San Francisco in the same category as New York, but with a growth pattern that shows an even more pronounced outward expansion in relative terms. As a result, coworking spaces in the CBD now make up 20% of the city’s inventory, down from 34% last year.

Then, in a tie for ninth place, we have three Southern CBDs: Miami, FL with neighboring Fort Lauderdale, FL, as well as Austin, TX. But, besides the fact that all of these cities have 12 coworking spaces in their business districts, they couldn’t have been more different in terms of evolution.

As an example, Miami showed a significant outward expansion by gaining flex spaces overall, but dropping three centrally located ones. Conversely, Fort Lauderdale maintained the same inventory level in the CBD, but lost three spaces further out, resulting in a slightly increased downtown focus. Meanwhile, Austin maintained the same distribution as last year with 20% of the offer concentrated in the central business district. However, it did so at the expense of 10 spaces throughout the city, one of which was in the CBD.

As we’re nearing the low double digits, there are naturally even more CBDs neck-and-neck in 10th place. Namely, Pittsburgh, PA; Oakland, CA; Dallas, TX; Boston, MA and San Diego, CA each had 11 coworking spaces in their central business districts.

Notably, Pittsburgh is the only new entry in the 2024 ranking, moving up one spot despite maintaining the same number of centrally located flex spaces. It owes its place in the top 10 to the evolution in other cities’ CBDs, rather than a significant change in the local coworking market. However, outside of the downtown area, flex space users in Pittsburgh do have 14 new offices to choose from. That represents the largest shift among these top markets with the share of CBD flex workspaces dropping from 50% to just 31%.

Albeit to a lesser degree, the same overall evolution pattern was present in the other four cities that tied for 10th place: Oakland added two new spaces overall, losing one central location in the process. Otherwise, Dallas, Boston and San Diego saw decreases in their downtown offers, as well as throughout their wider coworking markets.

Beyond the Downtown Buzz: Cities Where Coworking Goes Off the Beaten Path

Unlike traditional offices, coworking spaces often buck the trend of clustering in central areas as a more scattered approach allows them to capitalize on the business model built around flexibility. Thus, in some cities, this drew some interesting patterns on the coworking map.

For instance, despite being the third-largest coworking market overall, Atlanta, GA continues to show a low concentration of coworking spaces within its CBD. Specifically, although it inched up from last year’s 6%, the current 7% share of centrally located flex spaces is still the lowest in the nation, thereby signaling local coworking space users’ clear preference to avoid downtown traffic. Even so, there’s a relatively high concentration of coworking options from Tech Square through Midtown Atlanta. There are also similar hotspots in Perimeter Center, Cumberland, Buckhead and College Park.

San Antonio, TX was another city on this same extreme with its CBD home to only 8% of its total coworking inventory. Here, the most significant flex workspace clusters are in the Medical Center area, as well as near San Antonio International Airport and in the retail districts up in Far North Central.

Not to be outdone, Las Vegas, NV also spoils coworking users who want to avoid downtown commutes with a wide range of options. Additionally, in stark contrast to Atlanta and San Antonio, the distribution across the city is very balanced with no accentuated clusters. Most coworking spaces are also in densely populated residential areas.

In this annual CoworkingCafe series, we ranked U.S. central business districts by the size of their coworking space inventory. In addition to a current snapshot on the distribution of coworking spaces within the most important economic hubs, this second edition highlighted the most significant changes that took place since last year’s study.

Expert insights

What are the reasons behind the contraction seen in the number of coworking spaces across most top CBDs?

Like the greater office market in general, CBDs continue to be the hardest-hit in the office reshuffling. It’s no different here than what we see in the traditional office markets — especially with people’s growing reluctance to commute ever since the pandemic. For coworking, business districts with fewer residents seem to be at the greatest risk of a reduction.

Also, as to why the most significant contractions are seen in the top business hubs — a smaller inventory simply means less volatility. If a city is not a major coworking market to begin with, we can expect to see less fallout in CBDs too.

Read more…

We believe the trend that’s unfolding is more of a reshuffling of where the coworking locations are in a metro, rather than a market-wide reduction in space. We are already seeing signs of an uptick in prime urban locations outside of the actual CBD, as well as more ‘urban-suburbs,’ which tend to be mixed-use, more walkable hubs within a suburb — the idea here is these locations are simply closer to residents.

What is the significance of the year-over-year contractions seen in the number of coworking spaces across many top CBDs?

Changes brought by hybrid work continue to shape our lifestyles and priorities, and where one works and lives is increasingly dependent on commute times, access to transit-oriented development, social diversity, retail diversity and economic incentives.

In this context, the current 2023-2024 change is not statistically significant for any of the top markets — at least not yet. These fluctuations are within normal limits, and if anything, they seem to confirm that the paradigm that office markets track closely with workplace and residential trends continues to hold true.

Read more…

What explains the resilience of cities like Philadelphia, Washington, D.C.?

Philadelphia is a good example of how transit-oriented development and adaptive reuse projects create fertile ground for coworking too. In one of our recent reports Philadelphia was ranked 14th nationally by the number of office-to-apartment conversions, bringing brand-new residential space into the heart of the business district. Other market insights suggest a trend towards such flexible workspaces, with notable locations like WeWork at 1900 Market Street and Task Up at 104 S 20th Street offering tailored environments for productivity and collaboration. Moreover, the city’s wider office market has seen a mix of developments, with life science projects bolstering construction starts and flexible spaces maintaining their hold, despite a drop in investment volume.

Similarly, the number of coworking spaces in the Washington D.C. CBD can be explained by several factors. On one hand, the rise of remote work and the gig economy has increased the demand for flexible office arrangements, while startups and small businesses often find coworking spaces more affordable — especially in the CBD where space can be at a premium. On the other hand, flex workspaces provide a community environment where professionals can network and collaborate, which is particularly appealing in a politically-centric city like Washington D.C. Being in the CBD also means proximity to government buildings, major corporations, and transportation hubs, which is a significant draw for businesses.

Coworking spaces offer short-term leases and a variety of office setups that cater to all these needs. Numbers in these resilient cities indicate a robust market for flexible work environments, and this trend reflects the broader shift towards more dynamic and adaptable workspaces in urban centers.

CBDs with fewer coworking spaces have generally remained more stable, even when looking at cities with otherwise significant coworking inventories such as Atlanta or Seattle. What are the dynamics that set these cities apart from other top coworking markets?

As Seattle continues to urbanize and develop, the CBD area is becoming a prime location for coworking spaces, offering proximity to amenities, transport, and other businesses. These factors combined contribute to the prevalence of coworking spaces in Seattle’s CBD, reflecting broader trends in the workplace and economic landscape.

As for Atlanta, in terms of coworking subscriptions, virtual office prices remained at high, while dedicated desks dropped, and open workspaces stabilized. This reflects a growing trend towards flexible workspaces, driven by the evolving needs of businesses and professionals for agility and adaptability of pricing in their working environments.

What trends should we expect to see in the next years in terms of the distribution of coworking spaces within these cities of high economic importance?

The wave of adaptive reuse projects will undoubtedly have a positive impact, as proximity to work remains crucial for a flexible lifestyle and a pillar of a healthy work-life balance. The number of apartments scheduled for conversion from old office spaces increased from approximately 12,000 in 2021 to more than 55,00 by 2024 nationwide. Office conversions now represent 38% of the 147,000 apartments in future adaptive reuse projects.

So, our CBDs are being transformed as we speak, revitalizing downtown areas. As cities grow, we see a higher demand for flexible office spaces that can accommodate the diverse needs of startups, freelancers, and remote workers. The cost-effectiveness and networking opportunities that coworking spaces inherently provide also continues to be appealing for small businesses and entrepreneurs.

Methodology

- The data used for this study reflects the available coworking space inventory as of March 1, 2024, and only includes properties that were completed and open to the public.

- The analysis only included cities with three or more coworking spaces in their central business districts.

- The New York City data point included all five boroughs (the Bronx, Brooklyn, Manhattan, Queens and Staten Island).

- Definitions for the CBDs used were provided by Yardi Matrix Real Estate Intelligence Source, and area delimitations were traced by local real estate professionals.

Fair Use & Redistribution

We encourage and freely grant you permission to reuse, host or repost the images in this article. When doing so, we only ask that you kindly attribute the authors by linking to CoworkingCafe.com or this page so that your readers can learn more about this project, the research behind it and its methodology.