Flexible work continues to influence the professional landscape in the UK and Ireland, where coworking has established itself as a mainstay of the contemporary office ecosystem. As of Q3 2025, the region has a total of 4,315 coworking spaces, making it one of the most extensively networked markets in the world.

This report provides an overview of the coworking sector across the UK and Ireland, outlining the cities with the strongest adoption, prevailing price levels, and the major players shaping the market.

Leading Markets by Number of Coworking Spaces

Coworking Presence Concentrated in Major Urban Hubs

Reflecting a wide geographic reach supported by diverse regional markets, the UK accounts for 4,048 coworking locations, while Ireland contributes 267. Within the UK, coworking activity remains concentrated in the country’s largest urban centers, with capital cities serving as the main anchors for supply.

Greater London leads the way with 1,191 coworking spaces, a sizeable portion of the UK’s total inventory. Manchester follows as the most active regional hub counting 120 locations, while Glasgow leads Scotland and takes third place on the national podium, followed by Birmingham – with 68 and 67 flex workspaces, respectively.

Cardiff is the busiest Welsh coworking space market (coming in as the eighth largest in the wider UK). Meanwhile, in Northern Ireland, Belfast leads the way with 35 flex workspaces, sharing tenth place overall with Nottingham.

Over in Ireland, Dublin stands as the country’s coworking capital, hosting 126 spaces, which amounts to nearly half of all locations nationwide. The city’s concentration of startups, global firms, and remote professionals continues to make it the focal point of Ireland’s flexible office ecosystem.

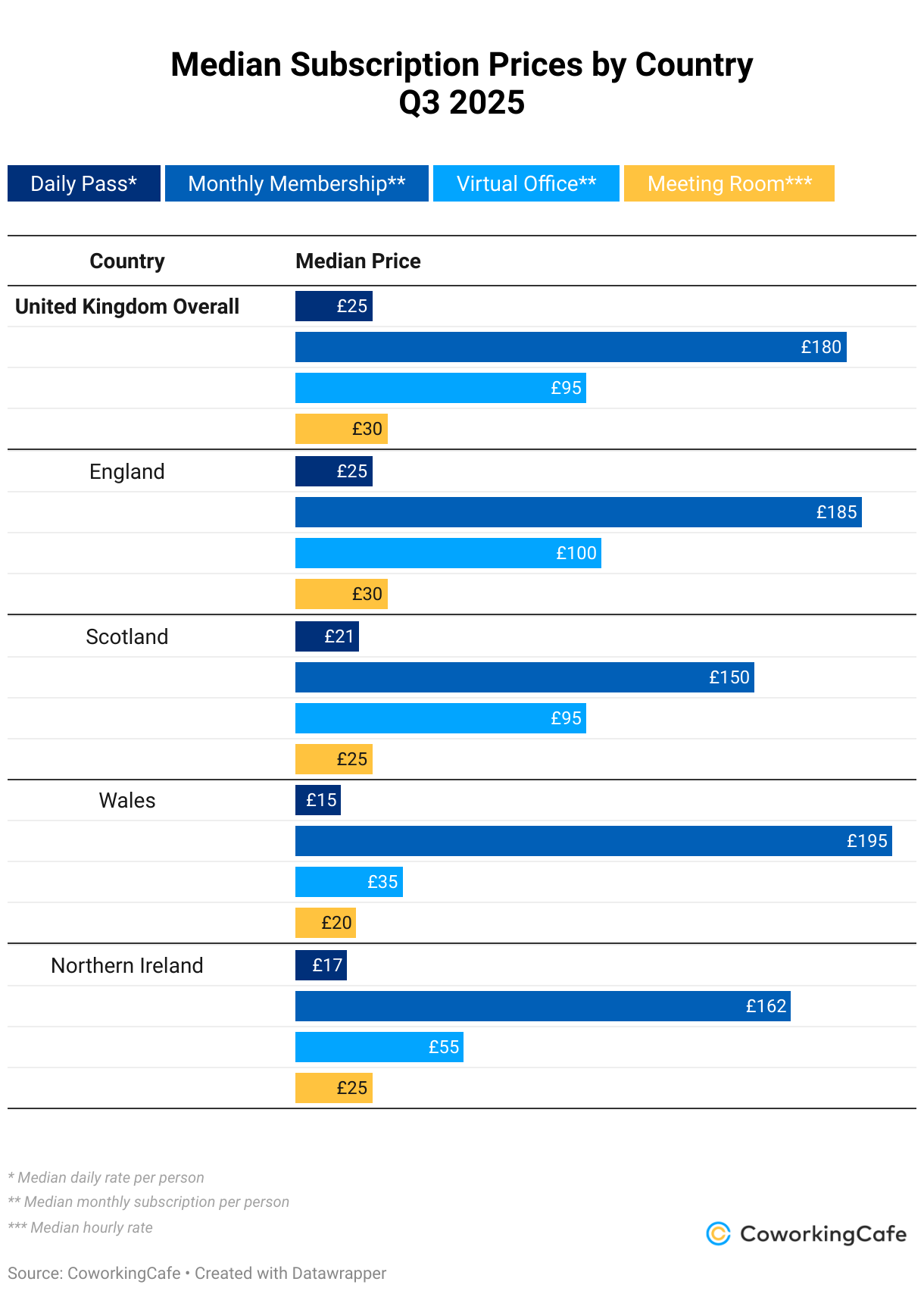

Coworking Subscription Prices

From Capital Premiums to Local Value: Coworking Prices on a Broad Spectrum

The UK’s coworking landscape features significant diversity in pricing, with core markets and secondary hubs showing distinct cost profiles. The following overview highlights the most and least expensive markets by median rates among the largest coworking powerhouses.

Day Passes

The median day pass price in the UK is £25, with higher-tier prices in Belfast, Oxford, Edinburgh, and Greater London – all tied at £30. Aberdeen also sits above the national midpoint at £28, while Birmingham, Leeds, and Liverpool each post median prices of £26.

At the other end of the range, Glasgow offers the most affordable day pass option among the top coworking markets at £20, followed by Bristol’s £21. Nottingham and Newcastle upon Tyne are tied for third place at a median rate of £23.

Monthly Memberships

The national median monthly membership stands at £180, reflecting broad accessibility across regions. Oxford’s £295 median price is by far the most expensive on this measure, followed by Brighton and Hove’s £207 and Greater London’s £200.

Other major markets such as Leeds (£197), Manchester (£195), Bristol (£195), Nottingham (£195), Edinburgh (£195), Cardiff (£194) and Belfast (£189) cluster closely around the national median. Liverpool and Aberdeen show the lowest median rates within the top group, both coming in at £139.

Virtual Office Services

The UK-wide median price for virtual office subscriptions lands at £95 per month. Birmingham and Glasgow occupy the upper tier with median monthly rates of £139, followed closely by Warrington with rates of £129. These three locations managed to outprice even Greater London and Liverpool – also neck-and-neck with £125.

Cardiff and Bristol offer the most economical options at £33 and £45, respectively, appealing to early-stage companies and remote professionals seeking a registered address without the expense of a physical desk.

Meeting Room Rentals

Meeting room prices vary widely by city, with the UK national median coming in at £30 per hour. Unsurprisingly, Greater London tops the list with £50, joined by Edinburgh and Manchester (both with median hourly rates of £35), and Birmingham’s £34 rounds out the podium.

Among the leading coworking markets, Nottingham and Glasgow offer the most affordable meeting room prices at £20 per hour. Meanwhile, Warrington, Leeds, Cardiff, Newcastle upon Thyne and Brighton and Hove are all in a tie for the second-lowest median rate, coming in at £25 per hour.

Coworking prices across Ireland vary modestly between Dublin and regional markets. The national median day pass is €25, compared to €32 in Dublin. Monthly memberships stand at €205 nationwide, aligning with the capital’s median. Virtual office subscriptions average €108 nationally and €149 in Dublin, while meeting room rentals register €40 nationally and €53 in the capital.

Top Operators Across the UK & Ireland

Regus Leads a Broadly Distributed Operator Landscape

In terms of operator presence, Regus holds top position in the UK and second spot in Ireland, reflecting the brand’s extensive national and international reach. With 193 coworking locations under the brand’s flag across the UK, including 71 within the top urban markets, Regus is present in just about every major city, underscoring its position as the most widely accessible flexible workspace operator in the region. By maintaining a diversified national footprint, rather than concentrating heavily in specific regions or market segments, Regus positions itself as the most widely available flexible workspace provider in the UK and Ireland.

Fora operates 64 locations nationwide, with 62 situated within the largest coworking markets. Its footprint is almost exclusively concentrated in Greater London, with only two regional outposts: one in Cambridge and one in Leeds. This selective, stability-focused strategy, clearly prioritizing market maturity, established demand and strong client bases, stands in sharp contrast to Regus’s broader, more risk-distributed approach.

Bruntwood, in third place, operates 69 locations nationwide, 54 of which across the top coworking markets. Roughly two thirds of its coworking portfolio is concentrated in and around Manchester, with additional sites in Cheshire, Liverpool, Leeds, Birmingham, London, and Cambridge. This regional focus centered on the North West (as well as their diversified strategy combining coworking spaces with science parks and innovation campuses) gives Bruntwood a distinct profile among major operators.

Next, Workspace Group holds 54 locations nationwide, 51 of which within the top markets – with a near-exclusive concentration in London, serving small and mid-sized businesses. Beyond the capital, its few sites in Bracknell, Woking, and Maidenhead share the same strategic logic: well-connected commuter hubs positioned just outside London’s core.

Completing the top five, Spaces operates 40 coworking locations in the top cities and 56 nationwide. Regus’ sister brand under the IWG umbrella, it combines a strong London base with selective coverage across major cities. With at least two spaces in all the major regional hubs, commuter-belt locations like Woking, Marlow, and Slough extend its reach beyond core metropolitan centers. This urban-and-peripheral strategy positions Spaces as IWG’s design-led, community-focused branch, offering flexible environments tailored to freelancers, startups, and growing teams.

In Ireland, Pembr leads the market with 19 locations. Pembr’s single-city strategy focuses on maintaining dense local coverage in Dublin, emphasizing brand visibility and consistency across central and suburban districts.

In second place, unlike Pembr, Regus maintains a national footprint, complementing its nine-strong capital presence with seven additional coworking spaces across Ireland – positioning itself as the only major operator with a truly national footprint.

Iconic Offices ranks third, focused exclusively on Dublin with 14 locations pursuing a premium, design-driven approach aimed at mature firms as well as startups seeking high-spec environments.

Methodology

- To compile this report, we used proprietary data from CoworkingCafe to determine the number of coworking spaces per market and the leading operators.

- The study relied solely on CoworkingCafe pricing data as of 29 September 2025 and inventory data as of 15 October 2025.

- Data was analysed at the city level with the exception of London (the City of London, plus 32 boroughs), based on built-up area (BUA) definitions as provided by the Office for National Statistics.

Sources:

– Office for National Statistics licensed under the Open Government Licence v.3.0 (contains OS data © Crown copyright and database right 2022)

– Northern Ireland Statistics and Research Agency licensed under the Open Government Licence v.3.0

- In terms of pricing, we looked at the national median starting prices per person per month for memberships and virtual office subscriptions; daily prices for day passes; and hourly rates for meeting rooms. Cities with three or fewer coworking spaces were excluded from the analysis.

Fair Use & Redistribution

We encourage and freely grant you permission to reuse, host or repost the images in this article. When doing so, we only ask that you kindly attribute the authors by linking to CoworkingCafe.com or this page so that your readers can learn more about this project, the research behind it and its methodology.