As hybrid work models continue to reshape the way many of us work, flexible office solutions are now an essential part of the business landscape. In particular, the UK and Ireland stand out as some of the world’s most dynamic coworking markets with an extensive network of spaces.

Coworking availability across the UK and Ireland stands at 4,199 locations in Q2 2025, placing the region among the most densely supplied flexible workspace markets globally. This large relative footprint is also evidence of a maturing sector shaped by sustained hybrid work adoption and robust demand for scalable, cost-efficient alternatives to traditional leases.

In this report, we examine the region’s flexible workspace ecosystem, focusing on the latest inventory figures, median prices, and the most active operators across leading UK and Irish markets.

Leading Markets by Number of Coworking Spaces

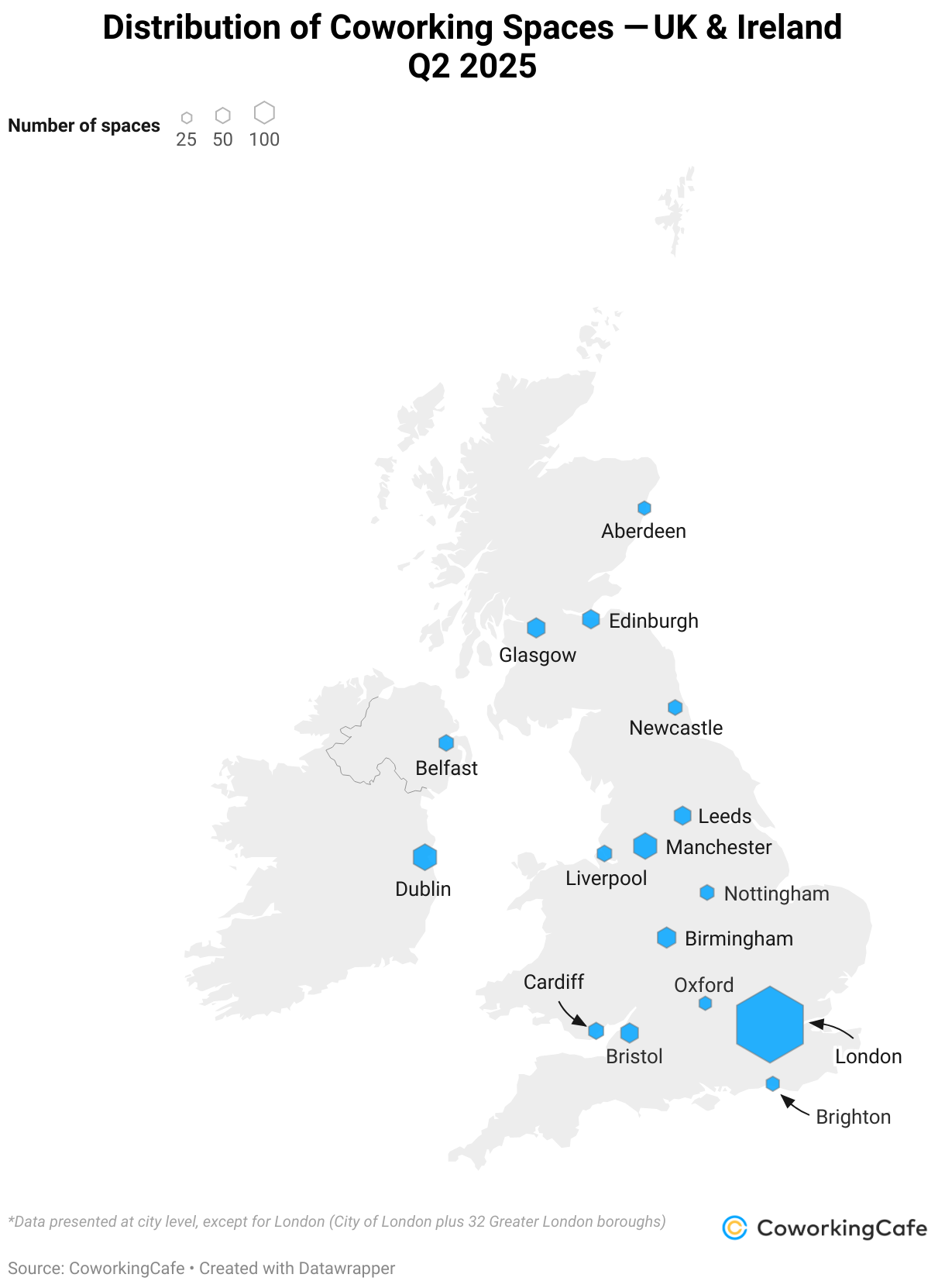

UK & Ireland’s Combined Inventory at 4,199, Heavily Clustered in Capital Cities

The UK is home to 3,949 coworking locations as of Q2 2025, while Ireland accounts for 250 with Dublin alone contributing nearly half of the country’s total.

Notably, nearly half of all UK flex office spaces (1,882) are clustered in the top 15 coworking hubs. Unsurprisingly, London’s magnetism for business makes it the crown jewel with 1,202 coworking spaces accounting for nearly one in three UK locations. Manchester ranks second with 118 coworking spaces.

Then, there’s a steep drop to the next tier of cities: Birmingham (68) rounds out the podium with Glasgow (61) leading Scotland neck and neck with Bristol (61) for fourth place on the UK-wide leaderboard. Not to be outdone, Edinburgh (55) and Leeds (54) hold strong mid-table positions, while Cardiff (41) stands out as the Welsh frontrunner. In Northern Ireland, Belfast leads with 38 coworking locations to tie with Liverpool.

Coworking Subscription Prices

Regional Price Gaps With Capital Premiums & Local Standouts

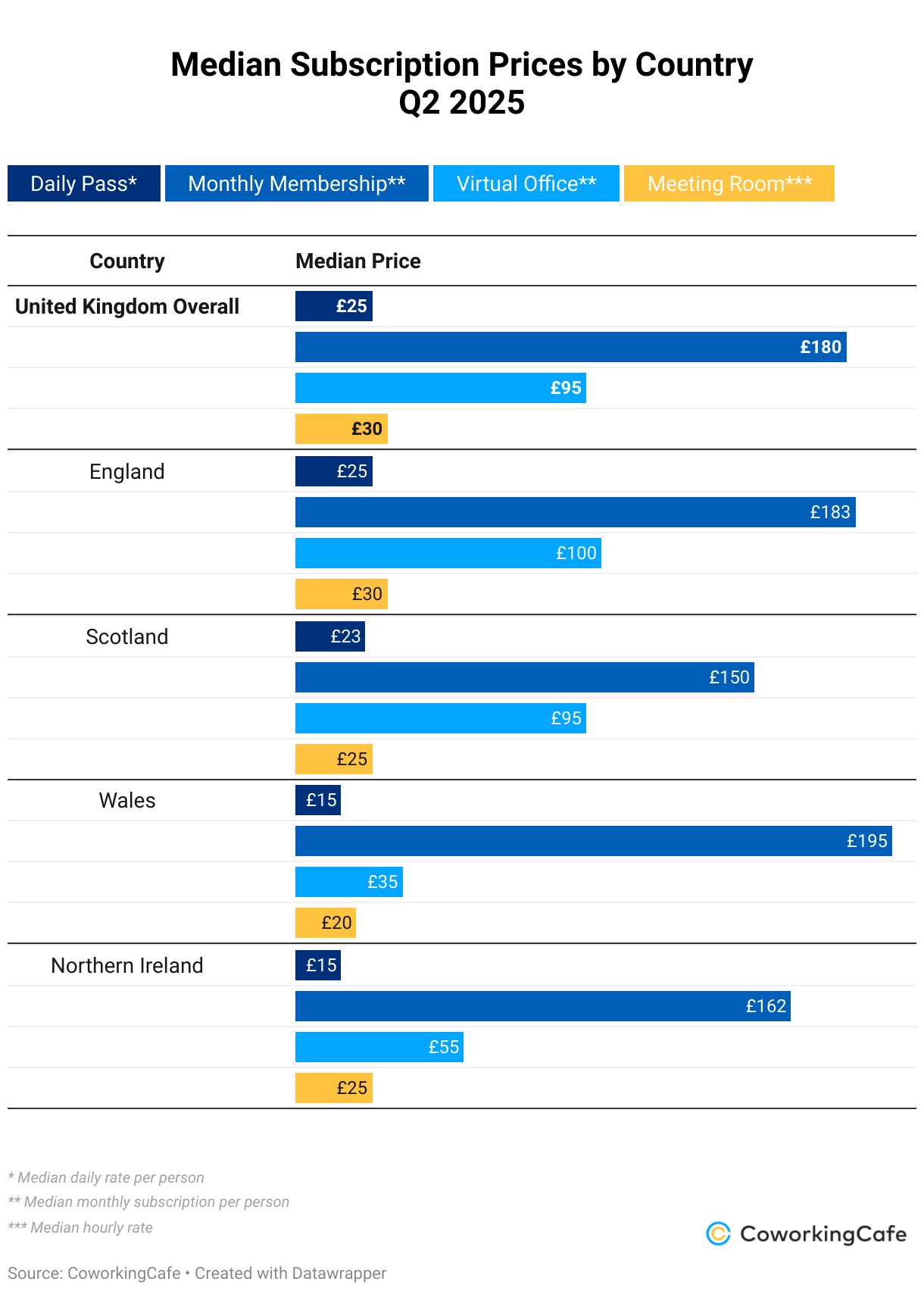

Coworking prices across the UK show wide regional variation, particularly between core markets and secondary hubs. To give a clearer picture of local pricing dynamics, below we highlight the highest and lowest median prices within the top 15 coworking markets.

Day Passes

The national median day pass price in the UK is £25, but several cities stand out with higher rates. At the top end, greater London, Oxford, Edinburgh and Belfast all report median day pass prices of £30. Aberdeen follows closely at £28, while Birmingham, Leeds and Liverpool each land just above the national median at £26.

On the more affordable side, Glasgow, Nottingham, Newcastle upon Tyne, and Brighton and Hove offer the lowest day passes at £23.

Monthly Memberships

Monthly open desk memberships across the UK come in at a median of £180, but several markets push well above that line. Once again, Oxford is in the lead with a striking £295 median, followed by Brighton and Hove (£207) and greater London (£203). Next, Leeds (£197); Manchester, Nottingham and Bristol (£195); and Edinburgh and Belfast (both £192) also register above-average rates.

Meanwhile, Liverpool records one of the lowest median prices in the top 15 markets at £139, followed by Birmingham with £150.

Virtual Office Services

Virtual office pricing shows even sharper disparities. The national median is £95 per month, yet Liverpool commands no less than £175. Greater London (£125), Glasgow (£119), and Birmingham (£114) all sit above the £100 psychological threshold.

In this case, Cardiff and Bristol are among the most affordable options in the top tier, offering virtual office services for less than £50 per month, thereby appealing to startups and remote teams with tighter budgets.

Meeting Room Rentals

Hourly rates for meeting rooms range widely with the national midpoint at £30. In this category, greater London tops the chart with a £50 median rate, followed by Edinburgh at £40. Next, Manchester and Birmingham both sit at £35 with Leeds just behind at £31.

It’s worth noting here that Glasgow and Cardiff offer some of the most affordable options at £23, and Nottingham comes in lowest among the top 15 coworking hubs at £20 per hour, making these cities ideal for organizations seeking budget-friendly meeting spaces.

Over in Ireland, Dublin holds a clear pricing premium across most coworking services. Here, the median day pass in the capital is €35, which is significantly higher than the €25 national median. Virtual office prices are also considerably higher, averaging €134 per month, compared to €117 nationally. Meeting room hourly rates follow the same pattern with a €50 median in Dublin — a €10 premium over the national level.

While monthly open workspace memberships in Dublin align with the national median of €205, the capital remains the most expensive market overall for flexible workspace in Ireland.

Top Operators Across the UK & Ireland

Regus Maintains Dominant Market Share

In terms of operator presence, Regus continues to lead the coworking market across both the UK and Ireland (although, in Ireland it shares the crown with Pembr). As of Q2 2025, the company operates 249 coworking spaces in the UK, including 90 locations within the top 15 urban markets — reflecting its wide national footprint and diversified presence. Within these top 15 markets, Fora ranks second by location count, operating 63 spaces (out of its 65-strong UK-wide portfolio) — underscoring a strategy concentrated in densely populated, high-demand urban hubs.

Beyond the top two, Bruntwood takes third place within the top 15 cities, with 53 locations out of a 69-site portfolio concentrated mainly in the North of England. The operator has built a strong regional presence by combining coworking with innovation campuses and enterprise support services — particularly in cities like Manchester, Leeds, Liverpool, and Birmingham. Then, Workspace Group follows closely with 51 locations in the top 15 cities and 54 across the UK overall, maintaining a near-exclusive focus on London and offering spaces tailored to small and mid-sized businesses. Rounding out the top five, Spaces operates 46 locations in the major markets and 63 nationally, leveraging the global IWG brand name to attract a mix of freelancers, startups, and enterprise teams.

In Ireland, coworking supply is overwhelmingly concentrated in Dublin’s dense and competitive market with the coworking scene outside of the capital being mostly dominated by small, independent providers with limited scale.

The top three operators — Pembr, Iconic Offices and Regus — all prioritize the capital. In fact, Pembr (18 locations) and Iconic Offices (14 spaces) are entirely concentrated in Dublin. For comparison, Regus maintains a more distributed approach by operating 10 of its 18 Irish coworking spaces in Dublin, thereby positioning itself as the only major operator with a truly national footprint.

Methodology

- To compile this report, we used proprietary data from CoworkingCafe to determine the number of coworking spaces per market and the leading operators.

- The study relied solely on CoworkingCafe inventory data as of 16 July 2025 and pricing as of 18 July 2025.

- Data was analysed at the city level with the exception of London (the City of London, plus 32 boroughs), based on built-up area (BUA) definitions as provided by the Office for National Statistics.

Sources:

— Office for National Statistics licensed under the Open Government Licence v.3.0 (contains OS data © Crown copyright and database right 2022)

— Northern Ireland Statistics and Research Agency licensed under the Open Government Licence v.3.0 - In terms of pricing, we looked at the national median starting prices per person per month for memberships and virtual office subscriptions; daily prices for day passes; and hourly rates for meeting rooms.

- Cities with three or fewer coworking spaces were excluded from the analysis.

Fair Use & Redistribution

We encourage and freely grant you permission to reuse, host or repost the images in this article. When doing so, we only ask that you kindly attribute the authors by linking to CoworkingCafe.com or this page so that your readers can learn more about this project, the research behind it and its methodology.