The coworking sector continues to mature and adapt as hybrid work drives a sustained demand for flexibility. And, with businesses across industries prioritizing adaptable, scalable office footprints, the first quarter of 2025 saw notable momentum in shared workspace growth. For a broader perspective, check out our Q4 2024 article to see how the trends have evolved.

Coworking Growth Stays Constant in Q1 as Southwest Florida, Brooklyn & San Antonio Lead the Charge

The U.S. coworking market kicked off 2025 with another solid quarter of growth: By the end of Q1, there were 7,840 coworking spaces nationwide — up 2% from the 7,695 recorded at the close of last year. This represents a net increase of 145 new coworking spaces, fueled by growth in both maturing urban hubs and emerging second-tier markets. Among the 50 tracked MSAs, 34 saw an increase in coworking inventory.

Use this interactive map to explore coworking trends across each region for Q1 2025!

Yet, some of the biggest gains didn’t come from the usual suspects. This time, the Southwest Florida Coast stood out with a 10% increase after adding four new locations to bring its total to 45. Brooklyn, NY, also made an impressive move by jumping 8% to 84 coworking spaces, while San Antonio posted a 7% boost to now sit at 64 locations. These kinds of gains are also showing up more and more in midsized markets as remote and hybrid workers look for local alternatives to the traditional office.

Meanwhile, Las Vegas also saw a solid bump, adding four new spaces for a 6% increase. Boston and Chicago both posted strong numbers — each growing 6% quarter-over-quarter. In fact, Chicago added 16 spaces to hit 279, coming within one spot of Manhattan’s 280. That’s a big step forward for a city that’s quietly becoming a powerhouse in the flex workspace world.

Coworking Prices Hold Steady — Unless You’re Going Virtual

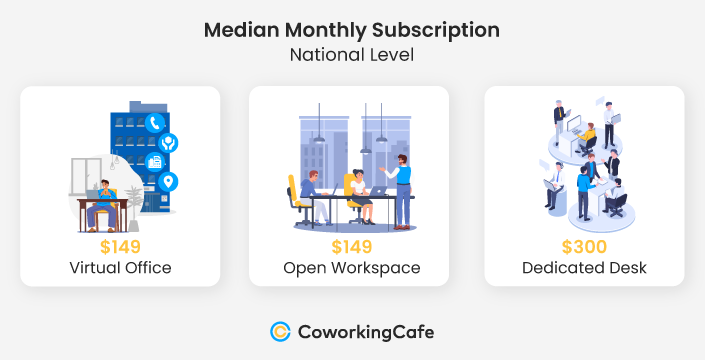

Coworking prices saw another quarter of mixed movement in Q1 2025: The national median for open workspaces held steady at $149 — the same as the previous quarter — but individual markets continued to move in different directions. In Manhattan, for example, open workspace rates jumped sharply, climbing from $240 to $339. On the flip side, Chicago saw its average fall to $125, down from $143 in Q4. That’s a meaningful shift, especially for a market that’s rapidly climbing the inventory ranks.

Other markets also saw solid increases in open workspace pricing. In particular, Los Angeles went from $160 to $185 and Washington, D.C. bumped up a bit from $163 to $175. Still, more than one-third of the markets tracked remained below the $149 national benchmark — especially in the Midwest and Southeast, where coworking remains a more budget-friendly option.

Other markets also saw solid increases in open workspace pricing. In particular, Los Angeles went from $160 to $185 and Washington, D.C. bumped up a bit from $163 to $175. Still, more than one-third of the markets tracked remained below the $149 national benchmark — especially in the Midwest and Southeast, where coworking remains a more budget-friendly option.

Dedicated desks followed a similar trend of scattered adjustments. Nationally, the median stayed put at $300, but some cities saw prices move significantly in either direction. That said, Manhattan, NY, remains the most expensive dedicated desk market, even after a small dip — from $519 down to $510.

Additionally, Denver and Nashville, TN, which had seen major increases last quarter, remained stable this quarter. At the same time, Chicago’s dedicated desk prices dropped from $287 to $269. That trend was echoed in other large markets, like Boston and Houston, where prices softened just slightly or remained steady.

But, the biggest story of the quarter came from the virtual office side. Nationally, median prices jumped from $120 to $149 — a substantial increase that signals stronger demand for remote business infrastructure. This is likely a reflection of businesses leaning more into hybrid setups and needing reliable mailing addresses and reception services without committing to physical space.

Despite the jump in median pricing, the price curve remained surprisingly flat in some markets. Namely, Washington, D.C. once again clocked in with one of the lowest virtual office rates at $80, just $1 more than last quarter. A few others — like Miami and Dallas-Fort Worth — also stayed below the $100 mark.

Leading Markets by Number of Coworking Spaces

LA and D.C. Hold Top Spots as Chicago Bridges Gap With Manhattan

At the start of 2025, the coworking leaderboard saw some subtle shifts while overall momentum continued to build. Los Angeles maintained its stronghold as the largest market by number of coworking spaces, expanding to 304 locations — up from 292 in the previous quarter. Washington, D.C. also posted solid gains, climbing to 286 spaces after adding nine new locations, enough to reach second place.

As a result, Dallas–Fort Worth dropped to third position after a modest 1% dip, bringing its total to 284. That drop also allowed Manhattan to regain ground after adding seven spaces to reach 280, narrowing the gap in the top tier of markets.

But perhaps the most notable move came from Chicago. The city added 16 coworking spaces in Q1 — the biggest numeric gain among all major metros — bringing its total to 279, just one shy of Manhattan. At this pace, Chicago is positioning itself as a serious contender for a top-three spot in upcoming quarters.

Leading Markets by Square Footage

U.S. Coworking Space Inventory Grows by Nearly 4 Million Square Feet in Q1 as Chicago, Tampa & San Antonio Stand Out

The national footprint of coworking spaces continued its upward trend in Q1 2025 with total allocated square footage reaching more than 140.7 million. That’s a 3% increase from Q4 2024, which closed at 136.9 million square feet — marking nearly 4 million square feet of additional flexible workspace across the country in just one quarter.

Leading the charge this time was San Antonio, which recorded a massive 18% jump in allocated space. More precisely, the city added more than 128,000 square feet, bringing its total to roughly 850,000. Otherwise, Chicago stood out among the largest markets with a 16% increase — adding more than 1.1 million square feet of coworking space to land at just above 8 million. That’s the biggest square footage boost among all major metros this quarter.

In Florida, Tampa-St. Petersburg-Clearwater also surged, growing by 14% to reach more than 1.73 million square feet — up from 1.53 million the previous quarter. Not to be outdone, White Plains, NY, also posted a strong 10% gain, climbing to nearly 680,000 square feet. Other large cities that posted notable increases included Boston (+8%); Pittsburgh (+7%); and Orlando, FL, (+6%).

Of course, not every market grew. Charlotte, NC, had the steepest decline of any major market, down 9% to 1.41 million square feet. Similarly, San Francisco saw a 6% drop in allocated space, falling to 3.43 million. Other markets with more modest declines included Dallas-Fort Worth (-3%); Sacramento, CA, (-3%) and Raleigh-Durham, NC, (-3%).

Average Coworking Space Size Inches Up in Q1, Led by Gains in White Plains, Pittsburgh & San Antonio

In Q1 2025, the national average size of coworking spaces ticked up slightly to 17,954 square feet — up 1% from 17,785 at the end of 2024. That modest increase keeps the trend of stabilization going as operators balance space efficiency with the demand for larger, more versatile layouts.

Interestingly, the biggest surprise this quarter came from White Plains, NY, where the average coworking space ballooned 15% to 10,617 square feet. While still on the smaller side in absolute terms, this marks a notable jump for a market outside the major metro spotlight. Next, Pittsburgh also saw a standout increase with a 12% gain pushing its average space to nearly 24,000 square feet. San Antonio wasn’t far behind, growing 11% to 13,274 square feet — a continuation of its strong quarter across multiple coworking metrics.

Among larger cities, Chicago led the way with a 9% increase, bringing its average up to nearly 29,000 square feet. Florida’s Tampa-St. Petersburg-Clearwater also saw a strong bump, rising 8% to more than 16,000 square feet. Other solid performers included Phoenix (+4.6%); Orlando, FL, (+4%) and Inland Empire, CA, (+4%).

However, Manhattan still held its position as the city with the largest average coworking footprint, even after a 2% dip brought it down to 40,429 square feet. Salt Lake City continued to stand out as well, averaging 23,680 square feet — up slightly from last quarter.

At the other end, San Francisco saw its average space size fall by 8% to 26,403 square feet. And, on the opposite coast, Brooklyn, NY, dropped even further — down 8.1% to more than 21,000. Charlotte, NC, Sacramento, CA, and Central Valley also recorded noticeable declines ranging from -3% to -6%. Dallas-Fort Worth lost ground as well, dipping 2.3% to just under 18,000 square feet.

That said, although the national shift was modest, the range of changes across cities tells a more complex story: Some markets are scaling up aggressively, while others continue to right-size based on local demand and economics. Either way, the overall picture suggests that coworking is settling into a smarter, more market-driven approach to space.

Distribution of Top Coworking Operators

Regus Holds Lead as HQ Posts Biggest Gains in Q1 Operator Expansion

The leading coworking operators — Regus, HQ, Industrious, Spaces and WeWork — continued to dominate the U.S. coworking landscape in Q1 2025. Together, these five brands expanded their nationwide footprint by 6%, growing from 1,720 total locations in Q4 2024 to 1,822 by the end of Q1. Furthermore, within the top 50 U.S. markets, the combined inventory of these providers rose by 4%, increasing from 1,501 to 1,554.

This quarter, HQ emerged as the fastest-growing brand among the top five. It added 26 new spaces in the top 50 markets — a 13% jump — and expanded its national count by 16% to reach 281 locations. This marks a strong push forward for the brand as it continues to scale across both large and mid-sized markets.

Spaces also had a solid quarter, growing its presence in the top 50 markets by 6% and nationwide by 5%, for 161 locations in total. That momentum reflects consistent demand for its sleek, corporate-friendly coworking environments.

Not far behind, Regus — still the largest coworking operator in the country — also saw healthy gains. Its national footprint grew by 5% to 1,073 spaces, while its top-market presence rose 2% to 871. In fact, Regus alone now accounts for nearly half of the coworking locations tracked among the top five operators.

Meanwhile, Industrious remained steady, with no change in its top 50 market total and just a 1% national gain—reaching 159 locations across the U.S. Lastly, WeWork held firm with 148 spaces both nationwide and in the top 50, registering zero change overall, though still maintaining a significant share of the market.

All told, these five providers now make up one quarter of the coworking spaces tracked nationwide — a clear indication that major players continue to drive the lion’s share of growth in the flex office sector. With the market expanding again this quarter and both new entrants and established players adjusting their strategies, the operator landscape remains one of the clearest indicators of where the industry is headed next.

Another great example is VAST Coworking, which continues to build momentum following its formation through the collaboration between Intelligent Office, Venture X, and Office Evolution. After ending 2024 with 175 locations, the network added two more spaces in Q1 2025, reaching a total of 177. The steady expansion of VAST underscores how large, multi-brand operators are capitalizing on market shifts — scaling their presence and signaling continued confidence in the long-term demand for flexible workspace.

Outlook: Steady Expansion With Focused Growth in Secondary Markets

The coworking landscape in Q1 2025 was shaped by a stable pace of national growth, increased adoption in midsized markets and rising square footage — all signs of a sector still in evolution, but on firm ground. As the industry looks to Q2 and beyond, demand from hybrid teams, solo professionals and enterprise clients will likely continue to drive expansion — not only in top-tier cities, but also across previously overlooked metros that are now playing catch-up in the flex office revolution.

What sets this quarter apart is the broader scope of the analysis: for the first time, our report covers the 50 largest coworking markets in the U.S., up from 25 in previous editions. This expanded view captures nuanced developments across the country, revealing how operators are responding to new patterns in remote work, economic migration and changing business needs.

Methodology

- To compile this report, we used proprietary data from CoworkingCafe to determine the number of coworking spaces per market, as well as the total square footage and leading operators.

- The study relied solely on the listing data available on CoworkingCafe as of April 2025.

- The top 50 markets analyzed were established by our sister company Yardi Matrix and were ranked based on allocated square footage.

- In terms of pricing, we looked at the national median starting prices per person per month for virtual office, open workspace and dedicated desk coworking subscriptions.

Fair Use & Redistribution

We encourage and freely grant you permission to reuse, host or repost the images in this article. When doing so, we only ask that you kindly attribute the authors by linking to CoworkingCafe.com or this page so that your readers can learn more about this project, the research behind it and its methodology.