As of Q1 2025, there are more than 4,000 coworking spaces operating throughout the UK and Ireland.

This places the region among the world’s most densely supplied coworking markets, which signals a widespread adoption of flexible and cost-effective workspace solutions, particularly among office-reliant industries shaped by hybrid and remote work models. By comparison, the U.S. inventory stands at just under 8,000 spaces — nearly double in absolute terms, but serving a population that’s more than four times larger.

This report provides an overview of the flexible workspace ecosystem by focusing on space supply across major markets, pricing structures and the most active markets in the region.

Leading Markets by Number of Coworking Spaces

UK & Ireland’s Combined Inventory at 4,090 Spaces

The UK leads the region with a total of 3,829 coworking spaces, while Ireland accounts for 261 locations as of Q1 2025. Notably, nearly half of the UK inventory is concentrated in just 15 key urban hubs, highlighting their central role in the global shift toward a more flexible work culture. In Ireland, this trend is even more pronounced — Dublin alone is home to nearly half of the country’s coworking spaces.

Moving closer, Greater London is clearly the epicentre with 1,145 coworking spaces, accounting for more than one in four UK flex workspaces. While London’s reign is cemented, Manchester’s total of 93 locations also leaves a significant gap for any city aiming to challenge its runner-up status. Then, despite its respectable, 63-strong inventory, Birmingham misses the national podium after landing between the two Scottish forerunners — Glasgow and Edinburgh with 67 and 58 spaces, respectively.

Beyond England and Scotland, Cardiff stands strong as the largest Welsh coworking market with 38 locations, while Belfast leads Northern Ireland with 32 spaces.

Coworking Subscription Prices

Pricing Trends Reflect Regional Variability

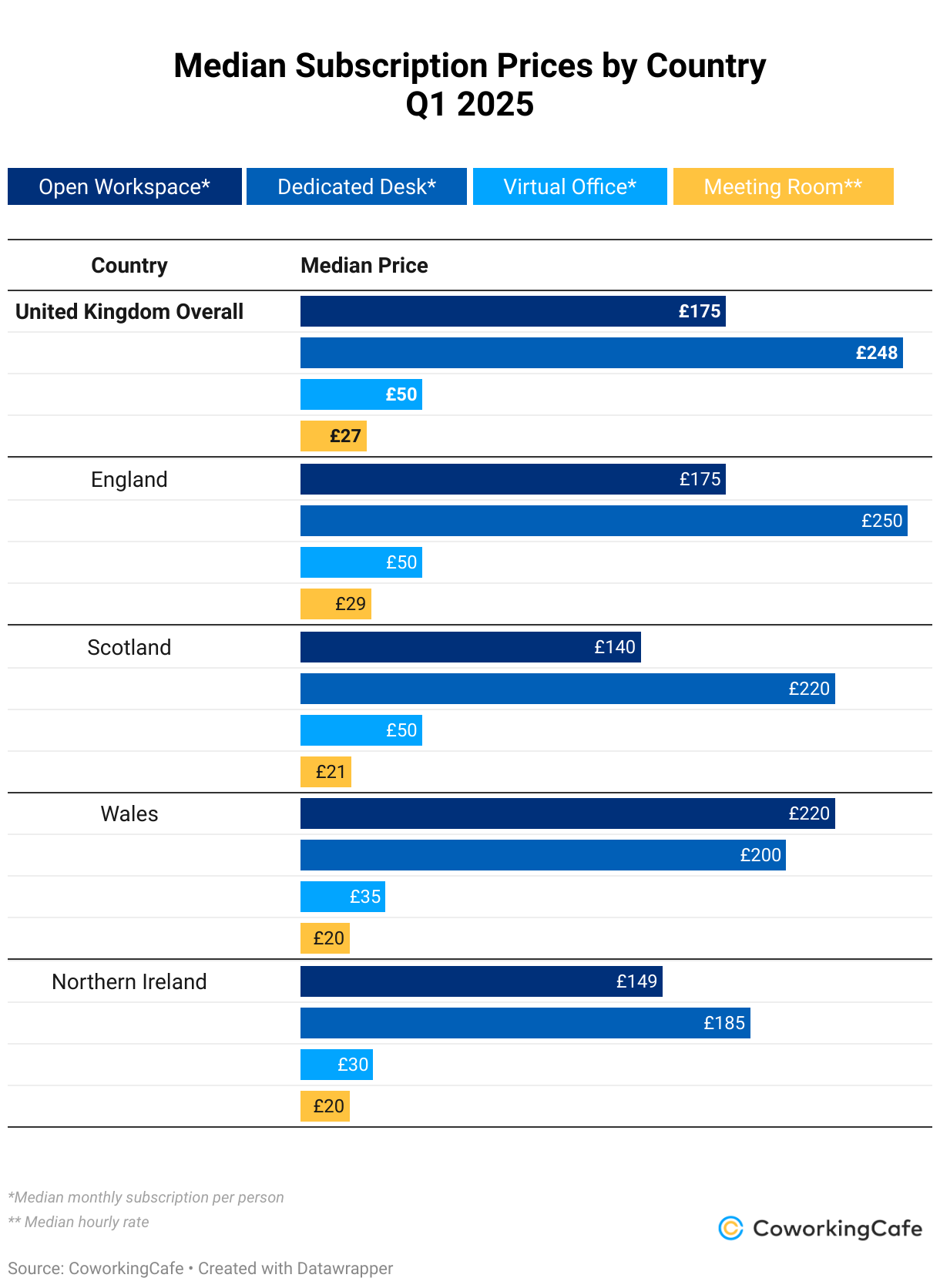

The pricing landscape for coworking spaces in the UK and Ireland shows significant regional differences. For instance, in the UK, the median monthly price of a dedicated desk is £248, whereas open workspace subscriptions come in at £175 per month and meeting rooms stand at £27 per hour. For fully remote businesses, virtual office memberships cost £50 per month.

Meanwhile, the combination of limited supply (29 spaces) and robust demand driven by its sought-after coastal location places Brighton and Hove at the top the UK’s dedicated-desk price chart with a £300 median monthly price. Albeit by a small margin, this pushes the capital to second place with the median price across London and its 32 boroughs clocking in at £297. Similarly, Oxford sets a high bar when it comes to open workspace memberships with a £295 median price, demanding a £45 premium compared to Greater London’s £250.

Of course, when it comes to meeting rooms and virtual office packages, London is back in the lead: Meeting rooms go for almost double the national median price, pegged at £50 per hour. Additionally, the capital’s prestigious addresses (with the additional remote business services) demand a £100 median monthly price in virtual office subscription fees. That said, Aberdeen is not far behind with similar solutions tagged at £95.

Dublin’s prices align with the Irish median for open workspaces at €200, but dedicated desks are slightly more expensive here, coming in at €299 per month — €4 above the national level. Meeting rooms are priced at €40 per hour (a €5 premium), while virtual office memberships reach a monthly €75, marking a €12 difference compared to the national median.

Distribution of Top Operators Within Largest Coworking Markets

Regus Maintains Strong Presence in UK & Ireland

In the UK, the coworking scene is shaped by a mixture of international giants and local operators. First, Regus takes the crown as the largest player, operating 198 locations across the UK and distinguishing itself with its location strategy as only 71 of its coworking spaces are concentrated in the most competitive markets.

Fora and Workspace Group follow closely with 63 and 53 locations, respectively, both focusing almost exclusively on Greater London.

Beyond the podium, WorkPad takes fourth place boasting 41 spaces, with Regus’ sister brand, Spaces, hot on its heels in fifth place with 39 coworking spaces.

In Ireland, Dublin’s coworking market is led by Pembr, Iconic Offices and Regus. Pembr operates all of its 18 locations in Dublin, while Iconic Offices manages 14 locations — also focusing exclusively on the capital. Not to be outdone, Regus (with a more diversified location strategy) runs 17 locations across Ireland, including its nine Dublin-based spaces.

Methodology

- To compile this report, we used proprietary data from CoworkingCafe to determine the number of coworking spaces per market and the leading operators.

- The study relied solely on CoworkingCafe inventory data as of 1 April 2025 and pricing as of 11 April 2025.

- Data was analysed at the city level, with the exception of London (the City of London, plus 32 boroughs), based on built-up area (BUA) definitions as provided by the Office for National Statistics.

Sources:

— Office for National Statistics licensed under the Open Government Licence v.3.0 (contains OS data © Crown copyright and database right 2022)

— Northern Ireland Statistics and Research Agency licensed under the Open Government Licence v.3.0 - In terms of pricing, we looked at the national median starting prices per person per month for virtual office, open workspace, and dedicated-desk coworking subscriptions and hourly rates for meeting rooms. Cities with three or fewer coworking spaces were excluded from the analysis.

Fair Use & Redistribution

We encourage and freely grant you permission to reuse, host or repost the images in this article. When doing so, we only ask that you kindly attribute the authors by linking to CoworkingCafe.com or this page so that your readers can learn more about this project, the research behind it and its methodology.